Chapter 1: Introduction

This book is a work in process.

It is my intent in this chapter to set up the topic, not as an introduction to a text book or course topic introduction, but rather as an integral introduction to the idea of cost accounting and challenges over time that lead to the development of cost accounting concepts or events that called them into question.

I am thinking at the moment of Josiah Wedgwood (Wedgwood pottery in the UK), in the late 1700s who, wrestling with a recession and trying to a cut costs while preserving his trained workforce, articulated difficulties in managing costs, particularly costs that stubbornly resisted cutting. His writings indicate he was wrestling with fixed costs and trying to understand them in order to manage them. There are other examples that can be called upon here, contained in research journals such as Accounting Organizations and Society.

The book Relevance Lost, The Rise and Fall of Management Accounting (Johnson and Kaplan, 1987) raise issues that students would benefit from being aware of, particularly how this book challenged the relevance of management accounting leading to the development of Activity Based Costing (Chapter 6), which was itself challenged in the Theory of Constraints (Goldratt, 1990).

I want to include a section on the Ford Pinto story. The Ford Pinto was prone to blowing up when struck from behind due to an exposed bolt that would be pushed into the gas tank, causing gas to leak out in an accident. Ford, using cost accounting techniques, concluded that the total cost of fixing the identified problem was more than the estimated costs (to Ford) of lives lost or impacted if nothing was changed (Gioia, 1992). In here too could be references to the story of the Corvair and Nader’s book, Unsafe at any speed (Nader, 1972).

Another articulation of the challenges of cost accounting could the Boeing 737 Max fiasco, where a culture of managing by numbers lead to the crash of two airplanes and the death of 346 people. The pilots fought the unexpected behavior of their airplanes, right up to the moment they plowed nose first into the ground. The pilots had no idea what was causing their their planes to nose dive. Boeing did. It was a software feature Boeing added to the 737 Max to compensate for the effect of the larger engines placed further forward on the standard 737 body. By classifying it as a minor change, the cost of training pilots on the feature was deemed unnecessary (Final Committee Report (2020).

I am not there yet though. But, it is good to have plans!

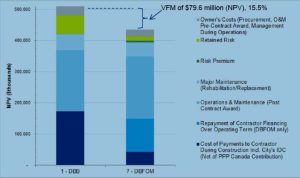

In Winter 2023 I do plan to use P3s in the introduction of the class, as an example of the misuse of cost accounting. Or, at very least an argument for a better understanding of costing accounting by the media and public. This will largely be based on (Bonner and Rennie, 2021). The graph below will be the critical focus.

(Deloitte, 2013)

Bill Bonner

References

Bonner, William (Bill), Rennie, M (2021). Public-Private Partnerships: What Counts as Evidence of Claimed Value?, In: Divided: Populism, Polarization and Power in the New Saskatchewan, edited by P. W. E. a. C. S. JoAnn Jaffe, Fernwood Publishing 2021. pp. 258-272. The graph in the text will be the critical focus.

Deloitte (2013) City of Regina Wastewater Treatment Plant Expansion & Upgrade Project Delivery Model Assessment, Deloitte, prepared for the City of Regina, 2013 Regina, Saskatchewan

Gioia, D.A. (1992). Pinto Fires and Personal Ethics: A Script Analysis of Missed Opportunities Journal of Business Ethics 1992 Vol. 11 Issue 5-6 Pages 379-389

Goldratt, E. M. (1990). The Theory of Constraints. Croton-On-Hudson, New York: North River Press, Inc.

Final Committee Report (2020): The Design, Development and Certification of the Boeing 737 MAX, US Congress, The House Committee on Transportation and Infrastructure September 2020

Johnson, H. T., & Kaplan, R. S. (1987). Relevance Lost: The Rise and Fall of Management Accounting. Boston, Mass: Harvard Business School Press.

Nader, R. (1972). Unsafe at Any Speed. New York, Grossman Publishers.