28 4.8 Using Variable Costing to Make Decisions

-

-

Last updated

- Dec 28, 2020

Learning Objectives

- Understand how managers use variable costing to make decisions.

In Chapter 2, we discussed how to report manufacturing costs and nonmanufacturing costs following U.S. Generally Accepted Accounting Principles (U.S. GAAP). Under U.S. GAAP, all nonmanufacturing costs (selling and administrative costs) are treated as period costs because they are expensed on the income statement in the period in which they are incurred. All costs associated with production are treated as product costs, including direct materials, direct labor, and fixed and variable manufacturing overhead. These costs are attached to inventory as an asset on the balance sheet until the goods are sold, at which point the costs are transferred to cost of goods sold on the income statement as an expense. This method of accounting is called absorption costing17 because all manufacturing overhead costs (fixed and variable) are absorbed into inventory until the goods are sold. (The term full costing is also used to describe absorption costing.)

Question: Although absorption costing is used for external reporting, managers often prefer to use an alternative costing approach for internal reporting purposes called variable costing. What is variable costing, and how does it compare to absorption costing?

-

-

Impact of Absorption Costing and Variable Costing on Profit

Question: If a company uses just-in-time inventory and therefore has no beginning or ending inventory, profit will be exactly the same regardless of the costing approach used. However, most companies have units of product in inventory at the end of the reporting period. How does the use of absorption costing affect the value of ending inventory?

-

-

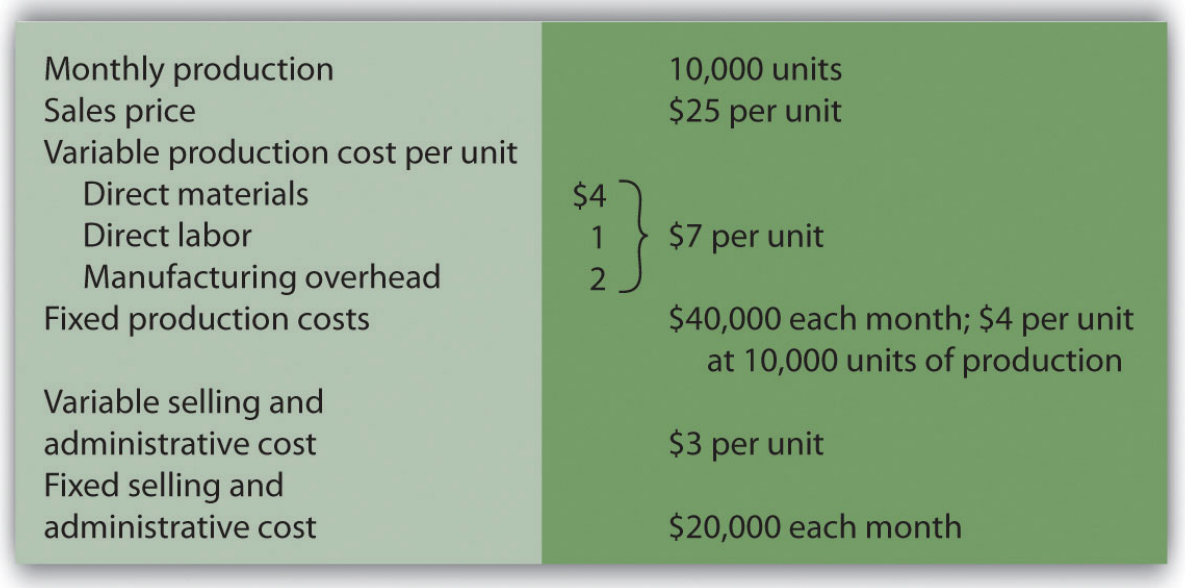

The following information is for Bullard Company, a producer of clock radios:

Assume Bullard has no finished goods inventory at the beginning of month 1. We will look at absorption costing versus variable costing for three different scenarios:

- Month 1 scenario: 10,000 units produced equals 10,000 units sold

- Month 2 scenario: 10,000 units produced is greater than 9,000 units sold

- Month 3 scenario: 10,000 units produced is less than 11,000 units sold

Month 1: Number of Units Produced Equals Number of Units Sold

Question: During month 1, Bullard Company sells all 10,000 units produced during the month. How does operating profit compare using absorption costing and variable costing when the number of units produced equals the number of units sold?

-

Month 2: Number of Units Produced Is Greater Than Number of Units Sold

Question: During month 2, Bullard Company produces 10,000 units but sells only 9,000 units. How does operating profit compare using absorption costing and variable costing when the number of units produced is greater than the number of units sold?

- Month 3: Number of Units Produced Is Less Than Number of Units Sold

Question: During month 3, Bullard Company produces 10,000 units but sells 11,000 units (1,000 units were left over from month 2 and therefore were in inventory at the beginning of month 3). How does operating profit compare using absorption costing and variable costing when the number of units produced is less than the number of units sold?

- Advantages of Using Variable Costing

Question: Why do organizations use variable costing?

-

-

Key Takeaway

As shown in Figure 4.8, the only difference between absorption costing and variable costing is in the treatment of fixed manufacturing overhead costs.

When comparing absorption costing with variable costing, the following three rules apply: (1) When units produced equals units sold, profit is the same for both costing approaches. (2) When units produced is greater than units sold, absorption costing yields the highest profit. (3) When units produced is less than units sold, variable costing yields the highest profit.

Review problem 4.8

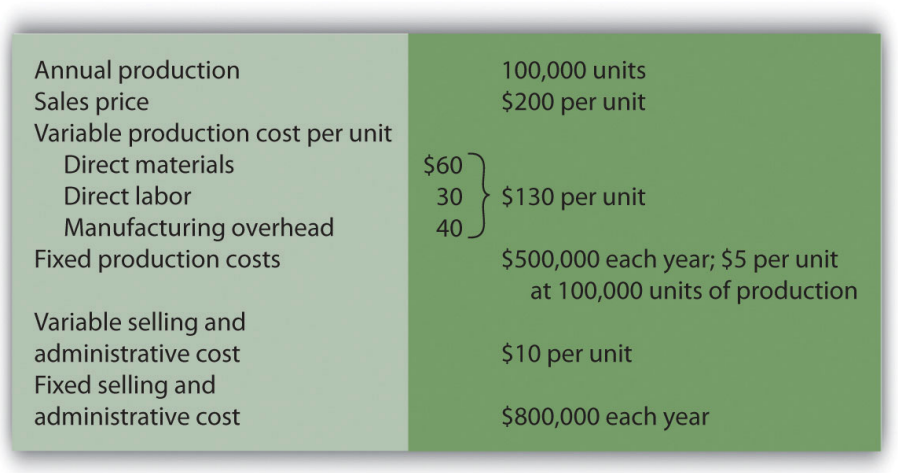

Winter Sports, Inc., produces snowboards. The company has no finished goods inventory at the beginning of year 1. The following information pertains to Winter Sports, Inc.:

- All 100,000 units produced during year 1 are sold during year 1.

- Prepare a traditional income statement assuming the company uses absorption costing.

- Prepare a contribution margin income statement assuming the company uses variable costing.

- Although 100,000 units are produced during year 2, only 80,000 are sold during the year. The remaining 20,000 units are in finished goods inventory at the end of year 2.

- Prepare a traditional income statement assuming the company uses absorption costing.

- Prepare a contribution margin income statement assuming the company uses variable costing.

Definitions

- A costing method that includes all manufacturing costs (fixed and variable) in inventory until the goods are sold.

- A costing method that includes all variable manufacturing costs in inventory until the goods are sold (just like

absorption costing) but reports all fixed manufacturing costs as an expense on the income statement when incurred.