53 7.5 Customer Decisions

-

-

Last updated

- Dec 28, 2020

Learning Objectives

- Use differential analysis to decide whether to keep or drop customers.

Question: Much like product line decisions, managers often use profitability as a determining factor to decide whether to keep or drop customers. This is an issue for all types of organizations, including manufacturers, retailers, and service companies. How does the differential analysis format differ for customer decisions compared to product line decisions?

Evaluating Customer Information

Question: Colony Landscape Maintenance provides services to three large customers: Brumfield, Hodges, and Orth. The segmented income statement in Figure 7.9 provides annual revenue and cost information by customer. Notice that this information is formatted similarly to the product line information in Figure 7.8. However, instead of tracking information by product line, here we track information by customer. Examine Figure 7.9 carefully and notice that the Brumfield account shows a loss for the year of $15,000. Should Colony Landscape Maintenance drop the Brumfield account?

Business in action 7.3 – Engineering Firm Fires Its Biggest Customer

The president of ABCO Automation, Inc., a 120-person engineering firm in North Carolina, decided it was time to fire the firm’s biggest client. Although the client provided close to 60 percent of the firm’s annual revenue, ABCO decided that firing this client was necessary. The president of ABCO stated, “We cannot be a great place to work without employees, and this client was bullying my employees. Its demands for turnaround were impossible to meet even with people working seven days a week. No client is worth losing my valued employees.”

The initial impact on revenues was significant. However, ABCO was able to cut costs and obtain new customers to fill the void. In addition, the fired client later gave ABCO two new projects on more equitable terms. The lesson from this is that dropping customers is not always a financial decision. ABCO’s client was profitable, but in the long run, the firm was at risk of losing valuable employees. This was a risk ABCO was not willing to take.

Source: Roger Herman and Joyce Gioia, “Herman Trend Alert,” Strategic Business Futurists 2004 (http://www.hermangroup.com).

Using Activity-Based Costing to Assess Customer Profitability

Question:

Key Takeaway

Managers use differential analysis to determine whether to keep or drop a customer. The format is similar to the differential analysis format used for making product line decisions. However, sales revenue, variable costs, and fixed costs are traced directly to customers rather than to product lines.

Review problem 7.4

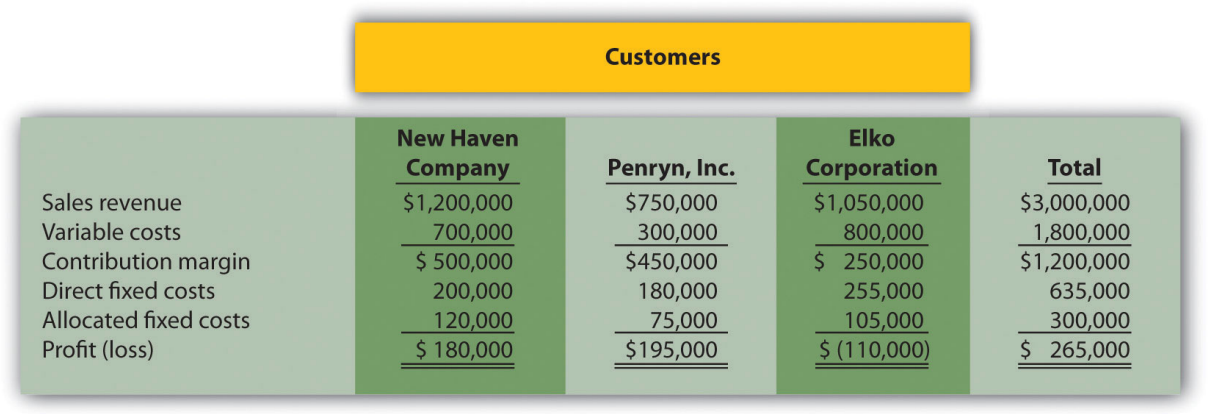

The following annual income statement is for Tatum & Associates, a firm that provides legal services to its customers.

Tatum & Associates is concerned about the losses associated with the Elko Corporation account and is considering dropping this customer. Allocated fixed costs are assigned to customers based on sales. For example, $105,000 in allocated fixed costs is assigned to Elko based on this customer’s sales as a percent of total sales [$105,000 = $300,000 × ($1,050,000 ÷ $3,000,000)]. If a customer is dropped, total allocated fixed costs are assigned to the remaining customers. All variable costs and direct fixed costs are differential costs.

- 1. Using the differential analysis format presented in Figure 7.10, determine whether Tatum & Associates would be better off dropping the Elko Corporation account or keeping the account. Explain your conclusion.

- Summarize the result of dropping the Elko Corporation account using the differential analysis format presented in Figure 7.12.