93 11.5: The Master Budget (Part 2)

-

-

Last updated

- Dec 28, 2020

Selling and Administrative Budget

Question: Now that the sales and production-related budgets are complete, it is time to estimate selling and administrative costs. What is a selling and administrative budget, and how is it prepared?

- Answer

Budgeted Income Statement

Question: Budgets completed to this point include sales (Figure 11.3), production (Figure 11.4), direct materials (Figure 11.5), direct labor (Figure 11.6), manufacturing overhead (Figure 11.7), and selling and administrative (Figure 11.8). Jerry’s Ice Cream now has enough information to prepare the budgeted income statement. What is a budgeted income statement, and how is it prepared?

- Answer

Question: How do companies use the budgeted income statement to improve operations?

Review problem 11.5

Carol’s Cookies estimates that all selling and administrative costs are fixed. Quarterly selling and administrative cost estimates for the coming year are

| Salaries | $60,000 |

| Rent | $ 7,000 |

| Advertising | $10,000 |

| Depreciation | $ 8,000 |

| Other | $ 1,000 |

- Prepare a selling and administrative budget for Carol’s Cookies using the format shown in Figure 11.8.

- Prepare a budgeted income statement for Carol’s Cookies using the format shown in Figure 11.9.

- Answer

Capital Expenditures Budget

Question: What is a capital expenditures budget, and how is it prepared?

- Answer

Cash Budget

Question: What is a cash budget, and how is it prepared?

- Answer

Cash Collections from Sales

Question: Assume all sales at Jerry’s Ice Cream are on credit. How long does it take, on average, for Jerry’s to collect on credit sales?

Cash Payments for Purchases of Materials

Question: Assume all purchases at Jerry’s Ice Cream are on credit. How long does it take, on average, for Jerry’s to pay for these credit purchases?

Other Cash Collections and Payments

Question: What other cash collections and cash payments must be considered at Jerry’s Ice Cream?

Review problem 11.6

Carol’s Cookies has the following information pertaining to the capital expenditures and cash budgets.

Capital Expenditures

The company plans to purchase selling and administrative equipment totaling $20,000 and production equipment totaling $28,000. Both will be purchased at the end of the fourth quarter and will not affect depreciation expense for the coming year.

Cash Budget

All sales are on credit. The company expects to collect 70 percent of sales in the quarter of sale, 25 percent of sales in the quarter following the sale, and 5 percent will not be collected (bad debt). Accounts receivable at the end of last year totaled $200,000, all of which will be collected in the first quarter of this coming year.

All direct materials purchases are on credit. The company expects to pay 80 percent of purchases in the quarter of purchase and 20 percent the following quarter. Accounts payable at the end of last year totaled $50,000, all of which will be paid in the first quarter of this coming year.

The cash balance at the end of last year totaled $20,000.

- Prepare a capital expenditures budget for Carol’s Cookies using the format shown in Figure 11.10.

- Prepare a cash budget for Carol’s Cookies using the format shown in Figure 11.11.

- Answer

Budgeted Balance Sheet

Question: The budgeted balance sheet is the last piece of the budget process. What is the budgeted balance sheet, and how is it prepared?

- Answer

Computer Application

Using Excel to Develop an Operating Budget

Managers often use spreadsheets to develop operating budgets. Spreadsheets help managers perform what-if analysis by linking the components of the master budget and automatically making changes to budget schedules when certain estimates are revised. For example, if managers at Jerry’s Ice Cream wanted to see what would happen if sales in units were decreased by 10 percent from the initial projection shown in Figure 9.3, they would simply reduce sales by 10 percent, and all budget schedules affected by this change would automatically be updated in the spreadsheet. An example of how to use Excel to develop an operating budget for Jerry’s Ice Cream follows. Notice the tabs at the bottom of the spreadsheet.

The first tab is for the sales budget worksheet, the second tab is for the production budget worksheet, the next tab is for the direct materials purchases budget worksheet, and so on. All these worksheets are linked so changes to certain estimates are reflected in the appropriate budget schedules.

Spreadsheet programs are not the only way managers use technology to facilitate the budgeting process. As indicated in Note 9.30 “Business in Action 9.2” the Web is also a useful tool when it comes to efficient budgeting.

Business in action 11.2 – Moving from Spreadsheets to Intranet Budgeting

The Pacific Northwest National Laboratory (PNNL) is one of nine multiprogram national laboratories of the U.S. Department of Energy. PNNL is operated by Battelle Science and Technology International, a global science and technology enterprise that conducts $3,000,000,000 worth of research and development annually.

The Facilities & Operations (F&O) Business Office at PNNL has over 130 budget activities, each of which requires an annual budget. The total annual budget is $70,000,000. Prior to 2000, activity managers were required to use Excel to process budget information. The F&O Business Office then uploaded this information to formulate the division’s budget.

As the F&O Business Office began the budget process for 2001, management decided to build a Web-based, or intranet, budget and planning system. The new system allowed managers to use the Web to input budget information directly, thus eliminating the need to upload initial budgets and subsequent budget changes.

Moving to intranet budgeting benefited PNNL’s F&O Business Office in several ways. Activity managers no longer had to use Excel to enter budget information, which saved 450 hours. The F&O Business Office saved 60 hours by no longer having to upload Excel budget information. Budget reports are easy to create, and the system provides real-time reports for analysis and project management.

Many organizations are adopting intranet budgeting as the primary source of planning and control. As the financial specialist at PNNL stated, intranet budgeting provides “a tool that is easy to use, accurate, and simple and will continue to save us time and money.”

Sources: Mary F. Astley, “Intranet Budgeting,” Strategic Finance, May 2003; Pacific Northwest National Laboratory, “Home Page,” http://www.pnl.gov.

Review problem 11.7

Assume Carol’s Cookies will collect 25 percent of fourth quarter budgeted sales in full next year (this represents accounts receivable at the end of the fourth quarter). The following account balances are expected at the end of the fourth quarter:

- Property, plant, and equipment (net): $320,000

- Common stock: $450,000

Retained earnings at the end of last year totaled $56,180, and no cash dividends are anticipated for the budget period ending December 31.

Prepare a budgeted balance sheet for Carol’s Cookies using the format shown in Figure 11.12.

- Answer

-

Wrap-Up of Chapter Example

The management group at Jerry’s Ice Cream is reconvening to discuss sales growth anticipated for the next budget period.

| Jerry: | Tom, I recall you saying we should expect growth between 10 percent and 25 percent next year. Have you been able to narrow this down a bit? |

| Tom: | Yes, I’ve talked with our salespeople and industry contacts. We also obtained trend data from a market research firm. Based on this information, sales should increase about 15 percent this coming year. Most agree this growth is a result of our high-quality product and our ability to quickly adjust flavors to accommodate consumer tastes |

| Jerry: | This is great news. It looks like our ice cream is really catching on |

| Michelle: | I received Tom’s projection a few days ago and already have a preliminary budget for next year. Lynn, you will have to do some serious planning to guarantee we have enough materials and employees for the third quarter spike in sales. |

| Lynn: | Yes, I realize we have some work to do to ensure we have enough resources to meet budgeted production levels. |

| Jerry: | Can’t we just hire a few more employees and let our suppliers know we will need more materials? |

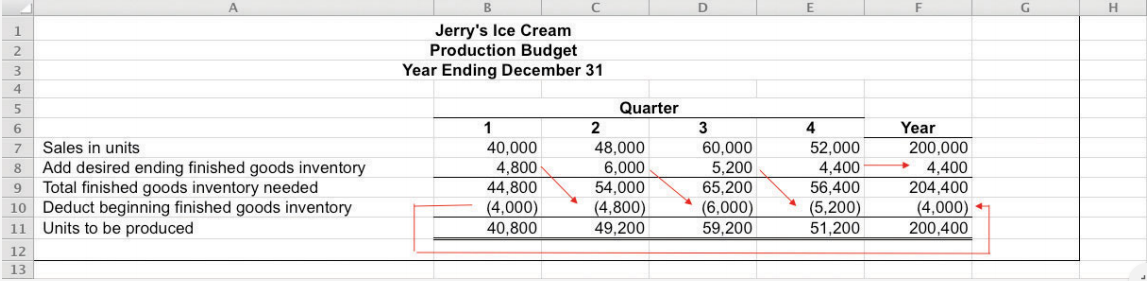

| Lynn: | The problem is that we have a spike in production during the third quarter. Production goes from 49,200 units in the second quarter to 59,200 units in the third quarter and back down to 51,200 units in the fourth quarter. I don’t think materials will be an issue—our supplier has already assured me this will not be a problem. But I can’t just hire new employees in the third quarter and fire them in the fourth quarter. |

| Jerry: | Perhaps our existing employees can work overtime, or we can hire temporary employees. |

| Lynn: | Hiring temporary employees would be my preference, particularly since college students are looking for part-time work during the summer months. Working overtime would really cause problems with our budgeted hourly rate of $13. |

| Jerry: | Michelle, do we have any cash flow problems with the anticipated growth? |

| Michelle: | Fortunately not. If all goes as planned, we should have more than $90,000 in the bank at the end of each quarter. |

| Jerry: | Excellent! Let’s do our best to stay on track. Michelle, I’d like an update at the end of the first quarter to see if actual profit meets or exceeds budgeted profit. |

| Michelle: | No problem. I’ll have it for you as soon as the books are closed for the first quarter. |

| Jerry | Now that we all have some idea of what to expect this coming year, we can make sure the resources are in place to make it happen. This should be an exciting and challenging year for us. Let’s meet again next month to discuss our progress in preparing for next year. |

This narrative provides an example of how the master budget is used for planning purposes. It is much more efficient to plan in advance for significant increases in sales and production than to wait and deal with production issues as they occur. The master budget can also be used for control purposes by evaluating company performance. We discuss the control phase of budgeting further in Chapter 11.

Key Takeaway

The master budget for a manufacturing company includes budget schedules for sales, production, direct materials, direct labor, manufacturing overhead, selling and administrative, the income statement, capital expenditures, cash, and the balance sheet. The sales budget is most important because sales projections drive the other budgets.

Definitions

- An estimate of all operating costs other than production.

- An estimate of the organization’s profit for a given budget period.

- An estimate of the long-term assets to be purchased during the budget period.

- An estimate of the amount and timing of cash inflows and outflows for the budget period.

- An estimate of the ending balances for all balance sheet accounts.