43 6.5 Using Activity-Based Costing to Allocate Overhead Costs (Part 2)

-

-

Last updated

- Dec 28, 2020

Comparison of ABC to Plantwide Costing at SailRite

After going through the process of allocating overhead using activity-based costing, John Lester (the company accountant) called a meeting with the same management group introduced at the beginning of the chapter: Cindy Hall (CEO), Mary McCann (vice president of marketing), and Bob Schuler (vice president of production). As you read the following dialogue, refer to Figure 6.7, which summarizes John’s findings.

| Cindy: | What do you have for us, John? |

|---|---|

| John: | I think you’ll find the results of our most recent costing analysis very interesting. We used an approach called activity-based costing to allocate overhead to products. |

| Bob: | I recall being interviewed last week about the activities involved in the production process. |

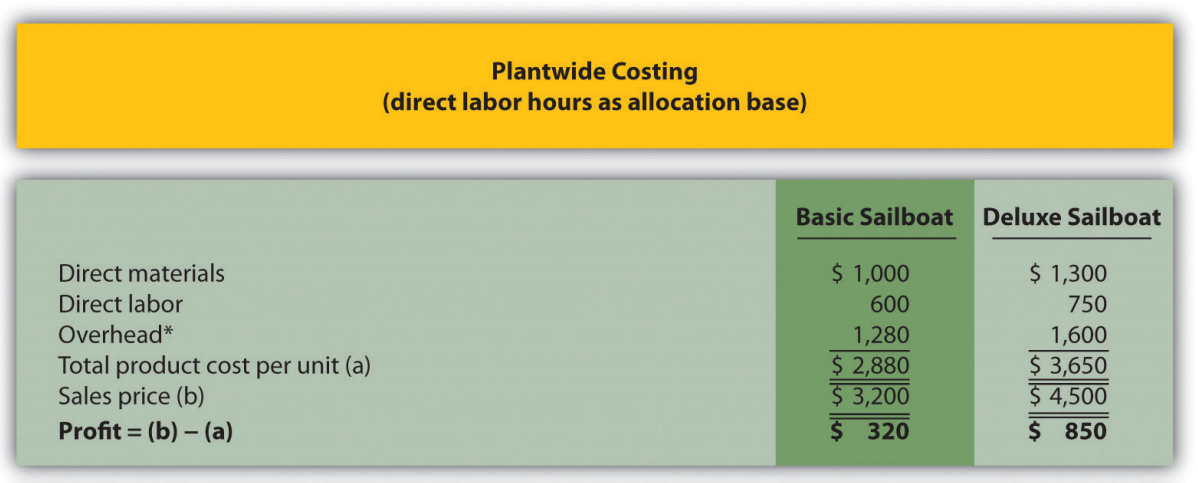

| John: | Yes, here’s what we found. The old allocation approach indicates that the Basic boat costs $2,880 to build and the Deluxe boat costs $3,650 to build. Our average sales price for the Basic is $3,200 and $4,500 for the Deluxe. You can see why we pushed sales of the Deluxe boat—it has a profit of $850 per boat. |

| Cindy: | John, from your analysis, it looks as if we were wrong about the Deluxe boat being the most profitable. |

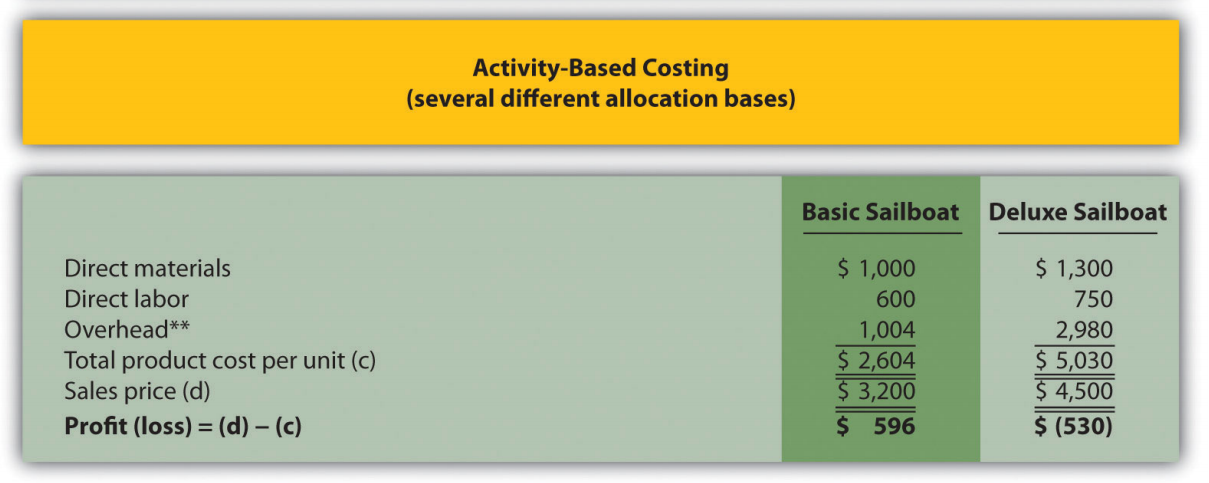

| John: | We do have some startling results. Using activity-based costing, an approach I think is much more accurate, the Deluxe boat is not profitable at all. In fact, we lose $530 for each Deluxe boat sold, and the profits from the Basic boat are much higher than we thought at $596 per unit. |

| Cindy: | I see direct materials and direct labor are the same no matter which costing system we use. Why is there such a large variation in overhead costs? |

| John: | Good question! When we used our old approach of one plantwide rate based on direct labor hours, the Deluxe process consumed 20 percent of all direct labor hours worked—that is, 50,000 Deluxe hours divided by 250,000 total hours. Therefore the Deluxe model was allocated 20 percent of all overhead costs. Using activity-based costing, we identified five key activities and assigned overhead costs based on the use of these activities. The Deluxe process consumed more than 20 percent of the resources provided for every activity. For example, running machines is one of the most costly activities, and the Deluxe model used about 44 percent of the resources provided by this activity. This is significantly higher than the 20 percent allocated using direct labor hours under the old approach. |

| Bob: | This certainly makes sense! Each Deluxe boat takes a whole lot more machine hours to produce than the Basic boat. |

| Cindy: | Thanks for this analysis, John. Now we know why company profits have been declining even though sales have increased. Either the Deluxe sales price must go up or costs must go down—or a combination of both! |

*From Figure 6.2

**From Figure 6.5.

Question: SailRite has more accurate product cost information using activity-based costing to allocate overhead. Why is the overhead cost per unit so different using activity-based costing?

-

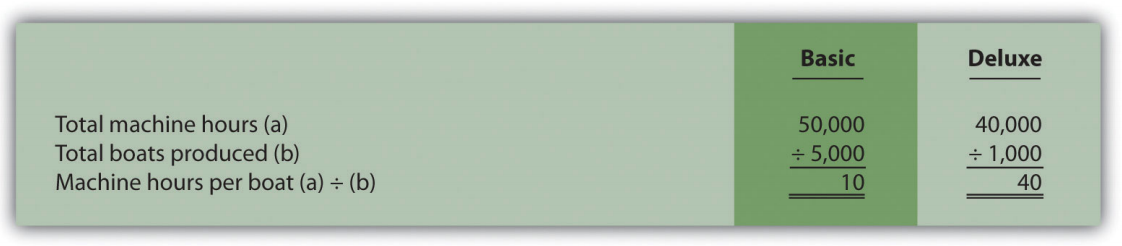

The primary reason that using activity-based costing shifted overhead costs to the Deluxe sailboat is that producing each Deluxe boat requires more resources than the Basic boat. For example, the Basic boat requires 50,000 machine hours to produce 5,000 boats, and the Deluxe boat requires 40,000 machine hours to produce 1,000 boats. The number of machine hours required per boat produced is as follows:

You can see from this analysis that the Deluxe boat consumes four times the machine hours of the Basic boat. At a rate of $30 per machine hour, the Deluxe boat is assigned $1,200 per boat for this activity ($30 rate × 40 machine hours) while the Basic boat is assigned $300 per boat ($30 rate × 10 machine hours).

Advantages and Disadvantages of ABC

Question: Activity-based costing undoubtedly provides better cost information than most traditional costing methods, such as plantwide and department allocation methods. However, ABC has its limitations. What are the advantages and disadvantages of using activity-based costing?

-

-

Business in action 6.1 – Characteristics of Companies That Use Activity-Based Costing

A survey of 130 U.S. manufacturing companies yielded some interesting results. The companies that used activity-based costing (ABC) had higher overhead costs as a percent of total product costs than companies that used traditional costing. Those using ABC also had a higher level of automation. The complexity of production processes and products tended to be higher for those using ABC, and ABC companies operated at capacity more frequently.

It is important to note that the differences between companies using ABC and companies using traditional costing systems in all these areas—overhead costs, automation, complexity of production, and frequency of capacity—were relatively small. However, users of ABC indicated their systems were more adequate than traditional systems in providing useful information for performance evaluation and cost reduction.

Source: Susan B. Hughes and Kathy A. Paulson Gjerde, “Do Different Cost Systems Make a Difference?” Management Accounting Quarterly, Fall 2003.

ABC Cost Flows

Question: How are overhead costs recorded when using activity-based costing?

-

Recap of Three Allocation Methods

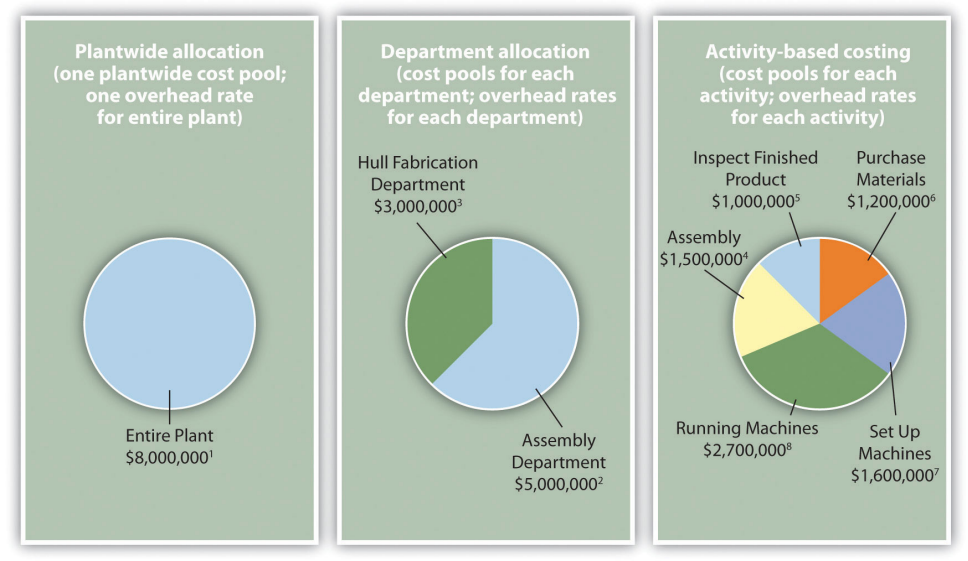

We have discussed three different methods of allocating overhead to products— plantwide allocation, department allocation, and activity-based costing. Remember, total overhead costs will not change in the short run, but the way total overhead costs are allocated to products will change depending on the method used.

Figure 6.9 presents the three allocation methods, using SailRite as an example. Notice that the three pie charts in the illustration are of equal size, representing the $8,000,000 total overhead costs incurred by SailRite.

Overhead Rates:

1 Allocated based on direct labor hours (DLH): $8,000,000 ÷ 250,000 DLH = $32 per DLH.

2 Allocated based on direct labor hours (DLH): $5,000,000 ÷ 217,000 DLH = $23 per DLH.

3 Allocated based on machine hours (MH): $3,000,000 ÷ 60,000 MH = $50 per MH.

4 Allocated based on direct labor hours (DLH): $1,500,000 ÷ 250,000 DLH = $6 per DLH.

5 Allocated based on inspection hours (IH): $1,000,000 ÷ 20,000 IH = $50 per IH.

6 Allocated based on purchase requisitions (PR): $1,200,000 ÷ 10,000 PR = $120 per PR.

7 Allocated based on machine setups (MS): $1,600,000 ÷ 2,000 MS = $800 per MS.

8 Allocated based on machine hours (MH): $2,700,000 ÷ 90,000 MH = $30 per MH.

Key Takeaway

Business in action 6.2 – Using Activity-Based Costing to Argue Predatory Pricing

BuyGasCo Corporation, a privately owned chain of gas stations based in Florida, was taken to court for selling regular grade gasoline below cost, and an injunction was issued. Florida law prohibits selling gasoline below refinery cost if doing so injures competition. Using a plantwide approach of allocating costs to products, the plaintiff’s costing expert was able to support the allegation of predatory pricing. The defendant’s expert witness, an accounting professor, used activity-based costing to dispute the allegation.

Both costing experts had to allocate costs to each of the three grades of gasoline (regular, plus, and premium) to determine a total cost per grade of fuel and a cost per gallon for each grade. Sales of regular grade fuel were significantly higher (63 percent of total sales) than the other two grades. Using the plantwide approach, the plaintiff‘s expert allocated all costs based on gallons of gas sold. Using the activity-based costing approach, the defendant‘s expert formed three activity cost pools—labor, kiosk, and gas dispensing. The first two cost pools allocated costs using gallons of gas sold and therefore were allocated as they would be with the plantwide approach (63 percent for regular grade, 20 percent for plus, and 17 percent for premium). The third cost pool (gas dispensing) allocated costs equally to each grade of fuel (i.e., one-third of costs to each grade of fuel). The gas dispensing pool included costs for storage tanks, all of which were the same size, as well as gas pumps and signs.

Compared with the plantwide approach, activity-based costing showed a lower cost per gallon for regular gas and a higher cost per gallon for the other two grades of fuel. Once the ABC information was presented, the case was settled, and the initial injunction was lifted.

Sources: Thomas L. Barton and John B. MacArthur, “Activity-Based Costing and Predatory Pricing: The Case of the Petroleum Retail Industry,” Management Accounting, Spring 2003; All Business, “Home Page,” http://www.allbusiness.com.

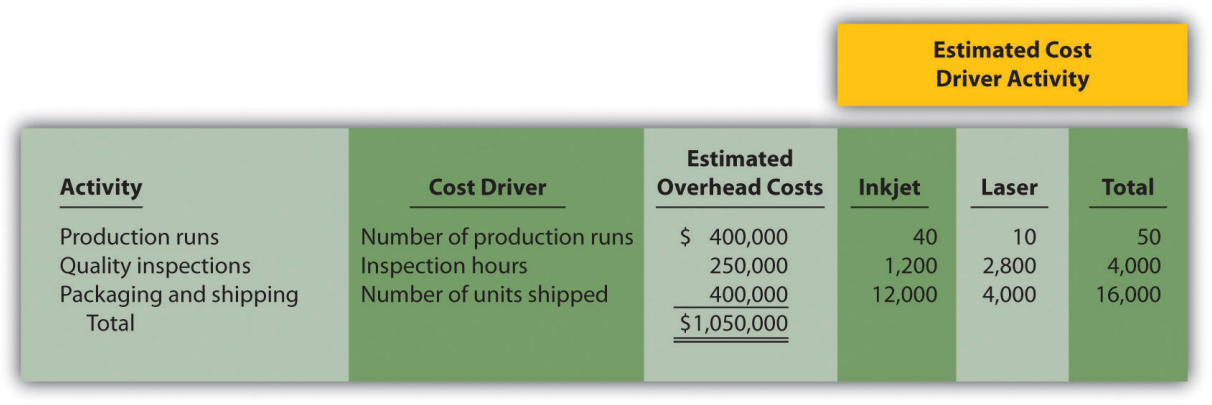

Review problem 6.3

Parker Company produces an inkjet printer that sells for $150 and a laser printer that sells for $350. Last year, total overhead costs of $1,050,000 were allocated based on direct labor hours. A total of 15,000 direct labor hours were required last year to build 12,000 inkjet printers (1.25 hours per unit), and 10,000 direct labor hours were required to build 4,000 laser printers (2.50 hours per unit). Total direct labor and direct materials costs for the year were as follows:

| Inkjet Printer | Laser Printer | |

|---|---|---|

|

Direct materials

|

$540,000 | $320,000 |

|

Direct labor

|

$600,000 | $400,000 |

The management of Parker Company would like to use activity-based costing to allocate overhead rather than use one plantwide rate based on direct labor hours. The following estimates are for the activities and related cost drivers identified as having the greatest impact on overhead costs.

Required:

- Calculate the direct materials cost per unit and direct labor cost per unit for each product.

- 1. Using the plantwide allocation method, calculate the predetermined overhead rate and determine the overhead cost per unit for the inkjet and laser products.

2. What is the cost per unit for the inkjet and laser products? - 1. Using the activity-based costing allocation method, calculate the predetermined overhead rate for each activity. (Hint: Step 1 through step 3 in the activity-based costing process have already been done for you; this is step 4.)

2. Using the activity-based costing allocation method, allocate overhead to each product. (Hint: This is step 5 in the activity-based costing process.) Determine the overhead cost per unit. Round amounts to the nearest dollar.3. What is the product cost per unit for the inkjet and laser products? - Calculate the per unit profit for each product using the plantwide approach and the activity-based costing approach. Comment on the differences between the results of the two approaches.