52 7.4 Product Line Decisions

-

-

Last updated

- Dec 28, 2020

Learning Objectives

- Use differential analysis for product line decisions.

Question: As competitors enter the market and as products go through life cycles, managers often must decide whether to keep or drop product lines. A product line4 is a group of related products. The Home Depot, Inc., has many different product lines such as appliances, flooring, and paint products. Ford Motor Co. produces a variety of products such as compact cars, trucks, and tractors. Companies must continually assess whether they should add new product lines, and whether they should discontinue current product lines.

Question: Notice that two lines appear for fixed costs: direct fixed costs and allocated fixed costs. What is the difference between direct fixed costs and allocated fixed costs?

Question: How are Barbeque Company’s allocated fixed costs assigned to individual product lines?

-

-

Question: Will dropping the charcoal barbecues product line result in higher company profit?

Misleading Allocation of Fixed Costs

Question: How can the charcoal barbecues product line show a loss of $8,000 in Figure 7.6, while the company as a whole is better off keeping this product line?

Including Opportunity Costs in Differential Analysis

Managers must often consider the impact of opportunity costs when making decisions. An opportunity cost7 is the benefit foregone when one alternative is selected over another. For example, assume you have the choice between going to school and working. The opportunity cost of attending school is the lost wages from working.

Question: In the case of Barbeque Company, assume the company can lease the space currently being used by the charcoal barbecues product line for $25,000 per year. Thus the opportunity cost (benefit foregone) of keeping the charcoal barbecues is $25,000. How does this affect Barbeque Company’s decision to keep or drop charcoal barbecues?

Sunk Costs and Differential Analysis

Question: What is a sunk cost, and how do sunk costs affect differential analysis?

-

-

Business in action 7.2 – Kmart Sells Stores

Source: Photo courtesy of Paul Sableman, http://www.flickr.com/photos/pasa/5583935536/.

The management of Kmart Corp., a mass merchandising company with more than 1,500 stores throughout the United States, agreed to sell 24 stores to Home Depot for $365 million in cash. Julian Day, Kmart’s president and chief executive officer, stated, “We will take advantage of opportunities to create value that include the sale of existing stores.”

In deciding whether to sell the stores, management likely considered the differential revenues and costs associated with keeping the stores versus selling them. Perhaps the stores were not profitable enough to exceed the $365 million in cash that Kmart received from the sale. Large retail companies with many widely dispersed stores commonly review their unprofitable stores on a regular basis and consider closing or selling stores that cannot turn a profit in the near future.

Source: Kmart Corp. press release, June 4, 2004 (www.kmartcorp.com).

Key Takeaway

Managers often us differential analysis to determine whether to keep or drop a product line. Direct fixed costs are typically eliminated if a product line is eliminated, and are considered differential costs. Allocated fixed costs are typically not eliminated if a product line is eliminated, and are not differential costs. Managers compare sales revenue and costs for each alternative (keep or drop), and select the alternative with the highest profit.

Review problem 7.3

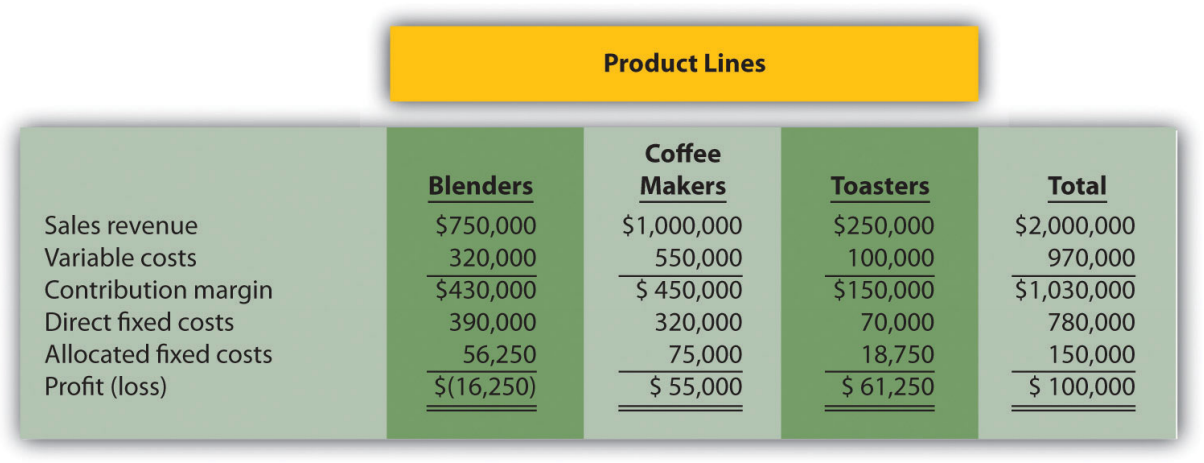

The following annual income statement is for Austin Appliances, Inc., a maker of electrical appliances:

Austin Appliances is concerned about the losses associated with the blenders product line and is considering dropping this product line. Allocated fixed costs are assigned to product lines based on sales. For example, $56,250 in allocated fixed costs is allocated to the blenders product line based on the blenders product line sales as a percent of total sales [$56,250 = $150,000 × ($750,000 ÷ $2,000,000)]. If Austin Appliances eliminates a product line, total allocated fixed costs are assigned to the remaining product lines. All variable costs and direct fixed costs are differential costs.

- Using the differential analysis format presented in Figure 7.6, determine whether Austin Appliances would be better off dropping the blenders product line or keeping the product line. Support your conclusion.

- Assume Austin Appliances can lease the warehouse space currently being used by the blenders product line for $15,000 per year. How does this affect the company’s decision to keep or drop the blenders product line?

- Summarize the result of dropping the blenders product line and leasing the warehouse space using the format presented in Figure 7.8.

Definitions

- A group of related products.

- Fixed costs that can be traced directly to a product line or customer.

- Fixed costs that cannot be traced directly to a product line or customer, and therefore are assigned to product lines or customers using an allocation process (also called common fixed costs).

- The benefit forgone when one alternative is selected over another.

- A cost incurred in the past that cannot be changed by future decisions.