4 2.4: Key Finance and Accounting Personnel

2.4: Key Finance and Accounting Personnel

Learning Objectives

- Describe the functions of key finance and accounting personnel.

Question: From the previous discussion, we know that planning and control functions are often designed to evaluate the performance of employees and departments of an organization. This often includes employees overseeing financial information. Thus it is important to understand how most large companies organize their accounting and finance personnel. What are the accounting and finance positions within a typical large company, and what functions do they perform?

Organizational Structure

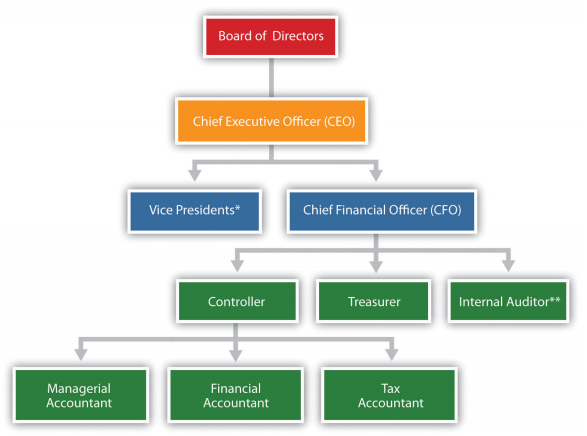

Figure 2.4 is a typical organization chart; it shows how accounting and finance personnel fit within most companies. The personnel at the bottom of the chart report to those above them. For example, the managerial accountant reports to the controller. At the top of the chart are those who control the company, typically the board of directors (who are elected by the owners or shareholders). Review Figure 2.4 before moving on to the detailed discussion of each important finance and accounting position.

*Represents vice presidents of various departments outside of accounting and finance such as production, personnel, and research and development.

**In addition to reporting to the chief financial officer, the internal auditor typically reports independently to the board of directors and/or the audit committee (made up of select members of the board of directors).

Chief Financial Officer

The chief financial officer (CFO) is in charge of all the organization’s finance and accounting functions and typically reports to the chief executive officer.

Controller

The controller is responsible for managing the accounting staff that provides managerial accounting information used for internal decision-making, financial accounting information for external reporting purposes, and tax accounting information to meet tax filing requirements. The three accountants the controller manages are as follows:

- Managerial accountant. The managerial accountant10 reports directly to the controller and assists in preparing information used for decision-making within the organization. Reports prepared by managerial accountants include operational budgets, cost estimates for existing products, budgets for new product lines, and profit and loss reports by division. (Note that some people use the term cost accountant interchangeably with managerial accountant. Others consider cost accounting a specific function of

managerial accounting that focuses on measuring costs. In this text, we use the term managerial accountant and assume that cost accountants focus on measuring costs.)

- Financial accountant. The financial accountant11 reports directly to the controller and assists in preparing financial information, in accordance with U.S. GAAP, for those outside the company. Reports prepared by financial accountants include a quarterly report filed with the Securities and Exchange Commission (SEC) that is called a 10Q and an annual report filed with the SEC that is called a 10K.

-

Tax accountant. The tax accountant12 reports directly to the controller and assists in preparing tax reports for governmental agencies, including the Internal Revenue Service.

Treasurer

The treasurer reports directly to the CFO. A treasurer’s primary duties include obtaining sources of financing for the organization (e.g., from banks and shareholders), projecting cash flow needs, and managing cash and short-term investments.

Internal Auditor

An internal auditor reports to the CFO and is responsible for confirming that the company has controls that ensure accurate financial data. The internal auditor often verifies the financial information provided by the managerial, financial, and tax accountants (all of whom report to the controller and ultimately to the CFO). If conflicts arise with the CFO, an internal auditor can report directly to the board of directors or to the audit committee, which consists of select board members.

Not All Organizations Are Alike!

Question: The organization chart in Figure 2.4 is intended to serve as a guide. However, all organizations are not the same, particularly smaller organizations. How might the organizational structure differ for a small organization?

Business in action 2.2 – The Organizational Structure of a Not-for-Profit Symphony

Financial limitations prevent a small not-for-profit symphony in California from hiring full-time finance and accounting employees. In spite of having annual revenues approaching $200,000, all financial transactions are processed and recorded by a part-time bookkeeper hired by the symphony. The bookkeeper also inputs budget information and provides monthly financial reports to the treasurer. The treasurer, a volunteer member of the board of directors, is responsible for establishing the annual budget and providing monthly financial reports to the board of directors. An outside firm prepares and processes all tax filings, assembles annual financial statements, and performs a review of the accounting operations at the end of each fiscal year.

Notice how the symphony does not have any of the formal positions identified in Figure 2.4, with the exception of the treasurer. This illustrates how financial constraints and reporting requirements may require an organization to be creative in establishing its organizational structure.

Key Takeaway

It is important to understand the key accounting and finance positions within a typical company and how each position fits into the organizational structure. The chief financial officer (CFO) oversees all accounting and finance personnel, including the controller, treasurer, and internal auditor. The controller is responsible for the managerial, financial, and tax accounting staff.

Review problem 2.3

For each of the six questions listed at the beginning of this section for Sportswear Company, determine who within the company would be responsible for providing the appropriate information. Assume Sportswear has the same organizational structure as the one shown in Figure 2.4.

Definitions

- A company whose shares of stock are publicly traded.

- The person in charge of all finance and accounting functions within the organization.

- The person responsible for managing the accounting staff that provides

managerial accounting information used for internal decision-making, financial accounting information for external reporting purposes, and tax accounting information to meet tax filing requirements.

- The person who assists in preparing information used for decision-making within the organization.

- The person who assists in preparing financial information in accordance with U.S. GAAP for external users.

- The person who assists in preparing tax reports for governmental agencies.

- The person responsible for obtaining financing, projecting cash flow needs, and managing cash and short-term investments for the organization.

- The person responsible for confirming that controls within the company are effective in ensuring accurate financial data.