41 6.3 Approaches to Allocating Overhead Costs

-

-

Last updated

- Dec 28, 2020

Learning Objectives

- Compare and contrast allocating overhead costs using a plant-wide rate, department rates, and activity-based costing.

Question: Managers at companies such as Hewlett-Packard often look for better ways to figure out the cost of their products. When Hewlett-Packard produces printers, the company has three possible methods that can be used to allocate overhead costs to products— plantwide allocation, department allocation, and activity-based allocation (called activity-based costing). How do managers decide which allocation method to use?

Plantwide Allocation

Question: Let’s look at SailRite Company, which was presented at the beginning of the chapter. The managers at SailRite like the idea of using the plantwide allocation method to allocate overhead to the two sailboat models produced by the company. How would SailRite implement the plantwide allocation method?

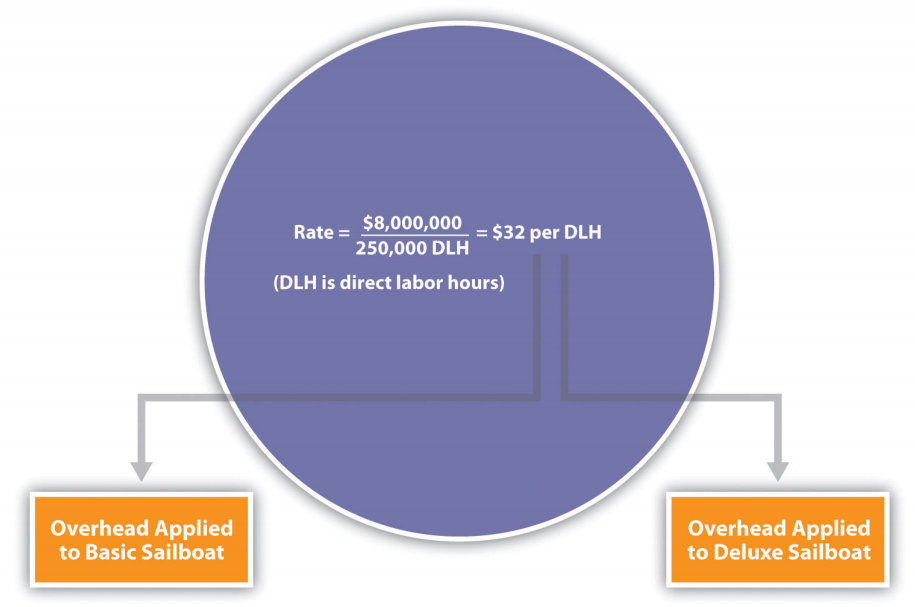

Using SailRite Company as an example, assume annual overhead costs are estimated to be $8,000,000 and direct labor hours are used for the plantwide allocation base. Management estimates that a total of 250,000 direct labor hours are worked annually. These estimates are based on the previous year’s overhead costs and direct labor hours and are adjusted for expected increases in demand the coming year. The predetermined overhead rate is $32 per direct labor hour (= $8,000,000 ÷ 250,000 direct labor hours). Thus, as shown in Figure 6.1, products are charged $32 in overhead costs for each direct labor hour worked.

Product Costs Using the Plantwide Allocation Approach at SailRite

Question: Assume SailRite uses one plantwide rate to allocate overhead based on direct labor hours. What is SailRite’s product cost per unit and resulting profit using the plantwide approach to allocate overhead?

Question: The managers at SailRite like the idea of using the plantwide allocation approach, but they are concerned that this approach will not provide accurate product cost information. Although the plantwide allocation method is the simplest and least expensive approach, it also tends to be the least accurate. In spite of this weakness, why do some organizations prefer to use one plantwide overhead rate to allocate overhead to products?

Department Allocation

Question: Assume the managers at SailRite Company prefer a more accurate approach to allocating overhead costs to its two products. As a result, they are considering using the department allocation approach. How would SailRite form cost pools for the department allocation approach?

The plantwide and department allocation methods are “traditional” approaches because both typically use direct labor hours, direct labor costs, or machine hours as the allocation base, and both were used prior to the creation of activity-based costing in the 1980s.

Key Takeaway

Regardless of the approach used to allocate overhead, a predetermined overhead rate is established for each cost pool. The plantwide allocation approach uses one cost pool to collect and apply overhead costs and therefore uses one predetermined overhead rate for the entire company. The department allocation approach uses several cost pools (one for each department) and therefore uses several predetermined overhead rates.

Review problem 6.2

Kline Company expects to incur $800,000 in overhead costs this coming year—$200,000 in the Cut and Polish department and $600,000 in the Quality Control department. Total annual direct labor costs are expected to be $160,000. The Cut and Polish department expects to use 25,000 machine hours, and the Quality Control department plans to utilize 50,000 hours of direct labor time for the year.

Required:

- Assume Kline Company allocates overhead costs with the plantwide approach, and direct labor cost is the allocation base. Calculate the rate used by the company to allocate overhead costs.

- Assume Kline Company allocates overhead costs with the department approach. Calculate the rate used by each department to allocate overhead costs.

Definitions

- A collection of overhead costs, typically organized by department or activity.

- A method of allocating costs that uses one cost pool, and therefore one predetermined overhead rate, to allocate overhead costs.

- A method of allocating costs that uses a separate cost pool, and therefore a separate predetermined overhead rate, for each department.